In A5 and B5, we explored how in vivo CAR-T is emerging not simply as a novel scientific idea, but as a possible answer to the structural problems of manufacturing, logistics, and access. In A6, we translated that trend into the patient perspective and examined why CAR-T is expensive and why it is often difficult to reach in practice. The next question, from a more technical and commercial standpoint, is where the real battle of CAR-T commercialization actually lies. The answer is not simply whether a company can make a powerful cell product. It is whether that product can be manufactured with reproducibility, delivered at acceptable cost, moved within acceptable timelines, and operated under an acceptable institutional burden. In that sense, CAR-T commercialization is not only a product-development challenge. It is also a competition in operating-system design.

The market’s increasing awareness of this systems problem is visible in the major transactions of the last year. AbbVie acquired Capstan in 2025, Kite acquired Interius in 2025, and Eli Lilly announced its acquisition of Orna Therapeutics on February 9, 2026. Lilly explicitly stated that Orna is focused on engineering immune cells in vivo, and the deal value was described as up to $2.4 billion including milestones. These transactions suggest that major players are no longer looking only for incremental efficacy gains. They are targeting alternative architectures that may address the classic bottlenecks of patient-by-patient manufacturing, long turnaround times, and limited treatment-center capacity. In other words, the competitive axis is shifting toward COGS, TAT, capacity, QC/CMC, site burden, and reimbursement readiness.

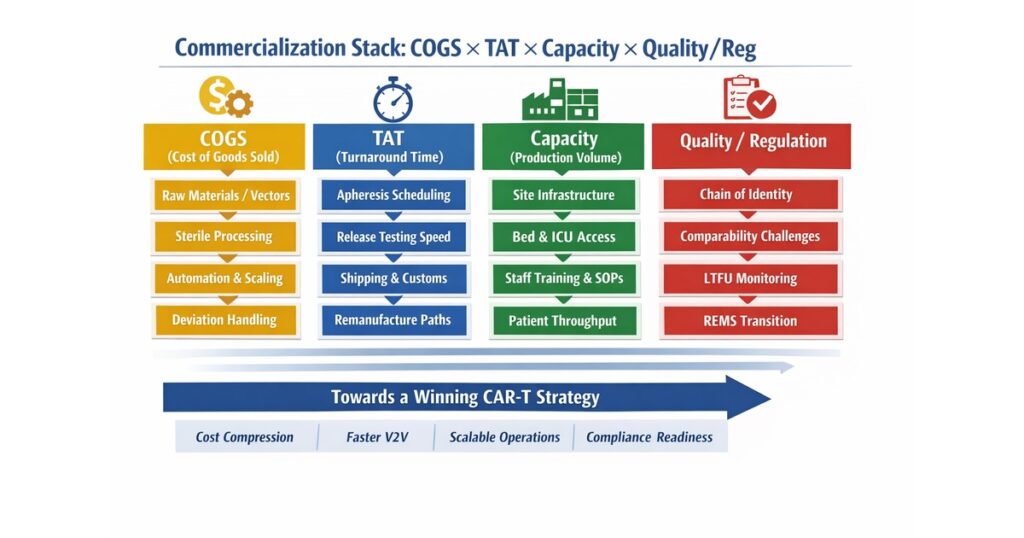

The First Metric in CAR-T Commercialization Is Not Revenue but “System Friction”

CAR-T is often discussed as a high-price therapy, but the price is not the core issue by itself. The deeper issue is that patient material collection, manufacturing, testing, transport, infusion, acute toxicity management, and long-term follow-up are linked into a single time-constrained chain. If one part of that chain jams, optimization elsewhere does not fully solve the problem. For commercialization analysis, it is therefore more important to ask where the platform creates friction than to start with list price or top-line revenue. Key friction points include the timing of apheresis, the need for bridging therapy, manufacturing failure rates, remanufacturing risk, release-test turnaround, transport conditions, ICU backup, and long-term follow-up obligations.

From this perspective, a commercial advantage in CAR-T cannot be defined merely by showing a strong response rate once infusion occurs. The more relevant question is how many eligible patients can actually be converted into infused patients. Vein-to-vein time is no longer just a manufacturing KPI. It is increasingly a clinical and economic KPI, because delays increase the risk that disease worsens before infusion and can alter the patient journey in ways that affect both outcomes and system cost.

COGS Is Not “the Cost of Making Cells” but the Total Cost of Individualized Manufacturing That Cannot Fail

When experts discuss CAR-T cost, one common mistake is to treat COGS as if it were mainly the cost of cell expansion. In reality, COGS includes raw materials, vector supply, sterile processing, labor, cleanroom and equipment burden, QC testing, deviation handling, logistics, scheduling, remanufacturing risk, and facility overhead. In autologous products, the fact that each batch is effectively a patient-specific lot is itself a structural driver of high cost. This is not a world where manufacturing variability can easily be averaged out through scale. Each patient comes with biological variability, yet each product still has to meet GMP expectations.

Among cost drivers, vector-related burden remains a major issue. The exact impact varies by platform and process design, but vector procurement, quality, and supply stability affect not only COGS but also capacity. Non-viral approaches, shorter expansion windows, and process simplification are therefore attractive routes for cost reduction. At the same time, low cost by itself is not enough. Reducing cost too aggressively can create new quality risks involving CAR expression, viability, cell composition, residual impurities, sterility, or replication-competent vector concerns. In practice, meaningful COGS reduction means identifying where standardization, automation, and step reduction can occur without breaking quality design.

The Real Value of Automation Is Not Labor Reduction but Variability Compression

Automation in CAR-T manufacturing is often described as a labor-saving measure. Its more important value, however, is that it can compress variability between operators, between facilities, and between process runs. A 2025/2026 Frontiers analysis showed that greater automation can reduce manufacturing costs by lowering personnel burden, cleanroom-grade requirements, and spatial footprint. But the deeper strategic benefit is that it helps create a manufacturing process that is more predictable at commercial scale.

Because CAR-T starts from biologically variable patient material, perfect uniformity is not realistic. Even so, closed systems, automated platforms, digital traceability, electronic batch records, and stronger in-process monitoring can reduce deviation rates and manual dependency. Commercial success in CAR-T is not about producing one excellent batch. It is about producing hundreds of batches under a disciplined process that remains interpretable, auditable, and scalable. In that sense, automation is not only a COGS strategy. It is also a regulatory-readiness strategy.

TAT and Vein-to-Vein Time Are Clinical Metrics Before They Are Commercial Metrics

One of the most important KPIs in CAR-T supply is turnaround time, and its practical clinical expression is vein-to-vein time. It matters because a slow TAT does more than reduce throughput. It reduces the probability that the patient will still be able to receive the product when it is ready. Recent analyses in myeloma and broader CAR-T settings have emphasized that short V2V time is critical, including from a health-economic perspective, because aggressive disease can progress during delay.

For this reason, “manufacturing capacity” should never be defined only as the number of batches a facility can run per year. A serious commercialization assessment must also include apheresis scheduling, slot flexibility, release-test turnaround, customs and shipping variability, backup paths for remanufacturing, and the ability of treatment centers to secure beds, drugs, and trained staff. In fast-moving indications such as CD19- or BCMA-driven disease, even a platform with slightly better product attributes can lose commercially if it loses on TAT.

In Cell Therapy, Supply Chain Is Not Mainly About Temperature Control but About Identity Control

The logistics of cell therapy differ fundamentally from ordinary pharmaceutical cold chain. In CAR-T, it is not enough to keep the material cold. The system must continuously prove whose cells these are, which process path they followed, under what conditions they were stored, and to which patient they are being returned. Chain of identity and chain of custody are quality issues, but they are also legal and regulatory issues.

That is why supply-chain design depends on uninterrupted data integrity across collection sites, manufacturing sites, and infusion centers. It also depends on understanding how changes in shipping mode, storage conditions, or cross-border transfer affect stability, comparability, and timing. A platform may have excellent biology, but if identity management is weak, commercialization becomes fragile. This point will not disappear with in vivo CAR-T or point-of-care manufacturing. If anything, more distributed models will make data traceability and digital integration even more important.

Release Testing Is One of the Most Underappreciated Commercial Bottlenecks

Many discussions focus on manufacturing itself, but in practice release testing can delay the entire chain. Sterility, identity, activity, viable cell count, transduction-related parameters, and related criteria all influence how quickly a product can move from manufacturing completion to infusion readiness. In commercialization terms, the key question is not simply how many tests are run, but which attributes truly function as critical quality attributes and how quickly they can be assessed reproducibly across sites.

The winning strategy here is not crude test elimination. It is rational test architecture. The field is moving toward better harmonization and faster readouts, but any shift in release logic has to remain defensible to regulators and connected to clinical relevance. That means release strategy is not a laboratory detail. It is part of platform design itself.

Comparability Is One of the Biggest Landmines During Scale-Up

Early-stage CAR-T development often prioritizes getting a product to work in patients. Once commercialization begins, however, process changes become unavoidable: equipment is upgraded, sites are added, materials change, freezing conditions are optimized, and assay methods evolve. At that point, comparability becomes one of the hardest problems in the field. Unlike conventional small molecules, cell products have multidimensional attributes, making it difficult to demonstrate that a changed product is still meaningfully “the same product.” FDA’s cellular and gene-therapy guidance framework remains a central reference point for this issue.

The commercial lesson is straightforward. If early development moves fast by using a process that cannot tolerate future change, the platform may stall badly at launch or during expansion. A winning B6-style strategy therefore requires building a process that can absorb future scale-out, analytical bridging, and multi-site deployment without collapsing under comparability pressure. This can look slower in the short term, but it is often stronger commercially in the long term.

Regulatory Change: REMS Removal Does Not Mean “Relaxed Safety,” It Means Transition to Mature Operations

A major regulatory shift occurred in June 2025, when the FDA eliminated REMS requirements for approved CD19- and BCMA-directed autologous CAR-T immunotherapies. FDA stated that the benefits and risks of these therapies could be managed without a REMS and that removing REMS would reduce unnecessary burden on the healthcare delivery system. This was a major change, but it should not be misunderstood as meaning that CAR-T safety management is no longer important.

What it really signals is that CAR-T is moving from a highly exceptional, tightly ring-fenced mode of operation toward a more mature model in which advanced but standardizable clinical workflows can support safe use. Treatment centers still need to recognize and manage CRS and neurotoxicity, maintain emergency-readiness, educate patients, and coordinate across specialties. For example, the October 2025 CARVYKTI prescribing information still instructs clinicians to monitor patients daily for at least 10 days following infusion and to have patients remain within proximity of a healthcare facility for at least 4 weeks after infusion. So the operational burden has not disappeared. It has been reframed.

From a commercialization standpoint, this means REMS removal should not be seen merely as a market-expansion event. The better question is how site education, standard operating procedures, and regional clinical networks can be redesigned to expand the treating-center base without degrading quality or safety.

Long-Term Follow-Up Remains a Heavy Obligation in Cell and Gene Therapy

Long-term follow-up remains a core issue for CAR-T and related gene-modified platforms. FDA’s 2020 guidance on long-term follow-up after administration of human gene therapy products remains an important anchor, and FDA continues to list it among its current cellular and gene-therapy guidance set. This reflects the fact that delayed safety signals, durable activity, and long-lived biological effects require observation beyond the acute treatment window.

From a commercialization perspective, LTFU matters not only because of regulatory burden, but because it introduces long-duration operational complexity into the post-approval model. Tracking patients over time, preserving data quality, handling relocation or transfer of care, linking with EHR or registry systems, and maintaining sponsor-site coordination all create cost and system load. For next-generation platforms, especially those involving in vivo delivery or potentially integrating systems, the scrutiny around long-term follow-up may become even more intense. That means platform value should be assessed not only on pre-approval clinical data, but also on whether the sponsor can actually operate the post-approval follow-up burden at scale.

Site Requirements Function Like Hidden Capital Expenditure

The problem of treatment-center readiness is often reduced to a distribution problem, but in reality it behaves more like human and institutional capital expenditure. Experienced physicians, nurses, pharmacists, coordinators, emergency-response pathways, bed access, proximity lodging, overnight support, and cross-specialty coordination all matter. Introducing CAR-T at a hospital is therefore closer to introducing a new care system than simply adding a new product.

This is why anything that makes the product easier to operate—shorter TAT, more predictable toxicity, shorter post-infusion observation burden, simpler monitoring—translates directly into broader site expansion potential. The strategic significance of commercial CAR-T therefore depends not only on approval, but also on whether hospitals realistically have enough implementation capacity to take the product on.

Pricing and Access Are Not Really About List Price, but About Payment-Model Design

CAR-T pricing is often framed as a question of whether the listed price is too high. For payers, however, the deeper issue is how to handle uncertainty around long-term benefit relative to very high upfront cost. This is why risk-sharing and managed-entry approaches continue to be discussed internationally for advanced therapies. The right question is not only how much the therapy costs, but in which patient groups it creates the most value, how that value should be measured, and how healthcare systems should bridge the time gap between immediate payment and long-term benefit.

In this framework, factors such as toxicity burden, readmission risk, need for bridging therapy, vein-to-vein time, and site-utilization burden are part of the economic story, not just the clinical story. A true winning strategy in CAR-T is therefore not just a strong efficacy package. It is a total value proposition that includes what the platform does to healthcare-system burden.

Why Major Pharma Is Rushing Into In Vivo CAR-T Now

Seen through the B6 lens, the recent interest in in vivo CAR-T becomes much easier to understand. The attraction of Orna, Capstan, and Interius is not simply that they are “more futuristic.” It is that they offer the possibility of redesigning the industrial architecture itself by reducing or bypassing apheresis, individualized ex vivo manufacturing, complex logistics, long vein-to-vein times, and treatment-center bottlenecks. Lilly is betting on Orna’s in vivo immune-cell engineering platform. The same broader strategic logic helps explain Capstan and Interius.

The March 25, 2026 Nature Medicine report on phase 1 anti-BCMA in vivo CAR-T adds to this momentum. The study reported that in five patients with relapsed or refractory multiple myeloma, in vivo generation of anti-BCMA CAR-T cells was feasible without leukapheresis, ex vivo manufacturing, or lymphodepleting chemotherapy, and no dose-limiting toxicities were reported in that tiny early cohort. That is encouraging, but it is still far too early to conclude that in vivo CAR-T will replace established platforms. The more realistic interpretation is that the field has entered a period in which legacy CAR-T optimization and next-generation implementation models will coexist and compete in parallel.

Allogeneic CAR-T and Distributed Manufacturing Remain Important Candidates for the “Winning Strategy”

In vivo CAR-T is not the only answer. Allogeneic CAR-T remains compelling because it aims to move away from patient-by-patient manufacturing. It carries its own biological challenges, including rejection, GVHD, and persistence, but from the standpoint of availability and standardization, it still represents a serious commercialization path.

Likewise, point-of-care or regionally distributed manufacturing models are becoming harder to dismiss, especially in discussions around access. The deeper point in B6 is not to declare one universal winner among centralized autologous manufacturing, distributed manufacturing, allogeneic platforms, and in vivo engineering. The more useful question is which model creates the least friction in a given indication, geography, reimbursement environment, and center-density setting.

So What Actually Defines a Commercial Winning Platform?

When all of this is assembled, commercially strong CAR-T companies and platforms tend to share a recognizable profile. They do not just reduce COGS; they design for COGS and quality at the same time. They shorten V2V and TAT in ways that are not only faster but also more predictable. They build QC, CMC, release logic, and comparability into the platform early rather than treating them as cleanup work later. They understand the burden on treatment sites and actively lower adoption friction. And they have a realistic plan for long-term follow-up and post-approval data capture.

Put differently, the winning strategy in CAR-T commercialization is not “making the most powerful cell once.” It is supplying a product of consistent quality, under regulatory scrutiny, in a way hospitals can operate, payers can tolerate, and patients can reach in time. If a legacy CAR-T platform can do that well, it may remain highly competitive. If an advanced next-generation design cannot do that, it may struggle despite scientific elegance. From the B6 perspective, CAR-T remains a biology race, but it is equally an operations race.

Conclusion: The Future of CAR-T Depends Less on “Stronger Cells” Than on “Systems That Actually Run”

The next decade of CAR-T will not be decided by response rate competition alone. Efficacy remains essential, but the decisive factors for commercialization are now becoming clear: how to compress COGS, how to shorten TAT, how to reduce site burden, how to design QC/CMC/comparability early, and how to manage long-term follow-up and payment structure.

In that sense, Orna × Lilly is not just acquisition news. It is a market signal about where the real competitive axis of CAR-T has moved. The same is true, more broadly, for the field’s increasing attention to alternative manufacturing and delivery architectures. Whether the future is dominated by improved conventional autologous CAR-T, allogeneic CAR-T, distributed manufacturing, or in vivo CAR-T, the eventual winner will be the side that can transform an expensive, complex, almost miraculous therapy into a reproducible, operable, real-world treatment system.

Comments