Key Takeaways

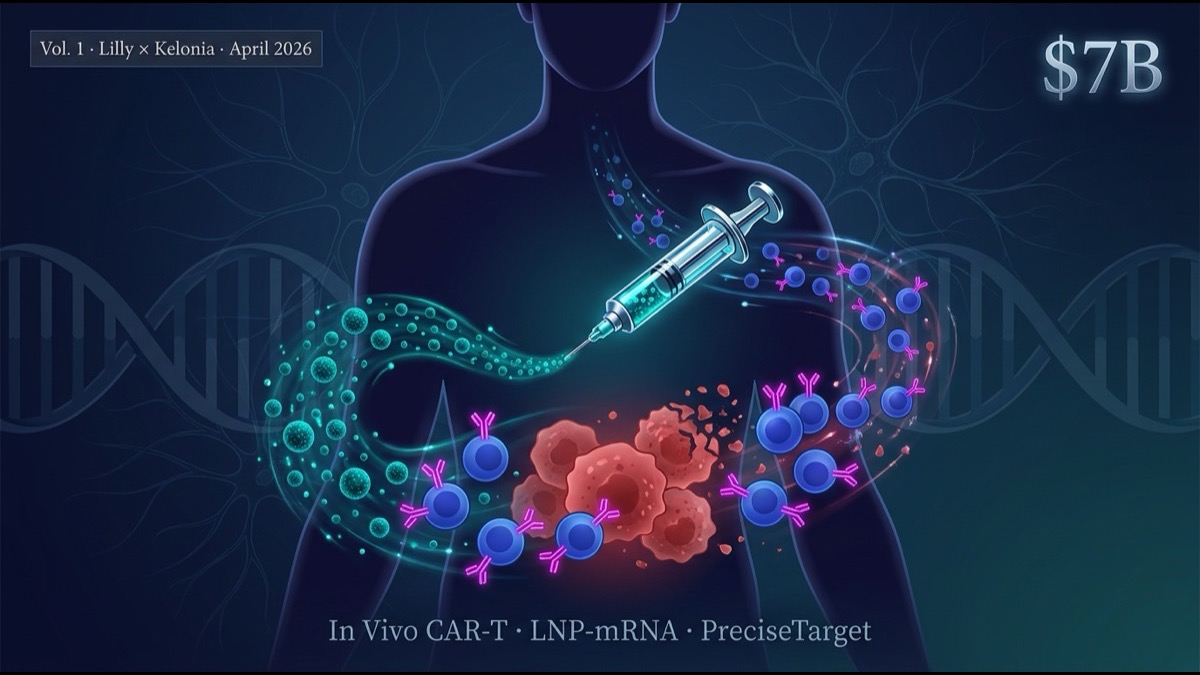

- On April 21, 2026, Eli Lilly signed a deal to acquire Kelonia Therapeutics for up to $7B ($3.25B upfront + milestones). This is Lilly’s second consecutive in vivo CAR-T acquisition of 2026 — on February 9, Lilly had already acquired Orna Therapeutics for up to $2.4B (circular RNA + LNP platform, autoimmune focus). Together, the largest in vivo CAR-T M&A run to date, signaling pharma majors entering the “next-generation gene therapy platform” race in earnest.

- Kelonia’s “PreciseTarget LNP” platform delivers cell-type-selective lipid nanoparticles directly to T cells (or hematopoietic stem cells) inside the patient, producing CAR expression in vivo via mRNA. This fundamentally differs from autologous ex vivo CAR-T, which requires apheresis, ex vivo gene editing, and expansion.

- Conventional CAR-T (Kymriah, Yescarta, Breyanzi, Carvykti, Abecma) faces three structural limits: (1) $400-500K/dose cost, (2) 2-4 week manufacturing time, (3) severe toxicity (CRS / ICANS). In vivo CAR-T can simultaneously soften all three.

- The impact on remaining independent competitors (Umoja, Renagade, Sana) is decisive. Note: Capstan was acquired by AbbVie for $2.1B in June 2025; Orna by Lilly in February 2026. With Lilly and AbbVie forming the two-camp oligopoly in in vivo CAR-T, valuations rise, partnership demand spikes, and talent flows accelerate across the field. Volume 2 dissects these competitors’ technical differentiation.

Introduction — The “Wait and Relapse” Problem of CAR-T

Chimeric antigen receptor (CAR) T-cell therapy has changed the landscape of cancer immunotherapy over the past decade. Kymriah (Novartis, 2017), Yescarta (Gilead, 2017), Breyanzi (BMS, 2021), Carvykti / Abecma (multiple myeloma, 2022) — successive approvals established CAR-T as treatment that saves patients with refractory B-cell lymphoma, ALL, and multiple myeloma who could not be saved by conventional chemotherapy.

But on the ground, three walls are well known:

- Manufacturing time: from apheresis → ex vivo genetic engineering & expansion → reinfusion takes 2-4 weeks. During this period, patients with progressive disease face a real risk of relapse / disease progression.

- Cost: autologous cell therapy requires patient-specific GMP manufacturing lines. The standard US payer price is $400-500K/dose — beyond what most insurance and societal systems can absorb at scale.

- Toxicity: cytokine release syndrome (CRS) and neurological toxicity (ICANS) occur in a meaningful fraction of patients, requiring inpatient and ICU management.

Over the past five years, the concept of “in vivo CAR-T” has emerged as a way to address all three simultaneously: generating CAR-T cells inside the patient’s body, without ex vivo manipulation, no patient-specific manufacturing line, and outpatient delivery. The concept was elegant; the technology was hard. Major M&A activity had been absent — until April 21, 2026.

2026 changed that — twice. Eli Lilly executed two consecutive in vivo CAR-T acquisitions: Orna Therapeutics on February 9 (up to $2.4B, circular RNA + LNP) and Kelonia Therapeutics on April 21 (up to $7B, lentivirus iGPS®). Two distinct modalities and two indication areas (autoimmune + oncology) acquired in rapid succession, lifting in vivo CAR-T from “concept” to “investment-grade asset” to “next-generation gene-therapy platform.” This article focuses on the Kelonia deal while situating it within Lilly’s broader 2026 acquisition arc.

Main Body

1. Who Is Kelonia?

Kelonia Therapeutics is a Boston-based biotech, founded in 2022. From inception, it has positioned itself as “the platform company that brings in vivo CAR-T to clinic”. It has been backed throughout by a16z Bio + Health, ARCH Venture Partners, and the Flagship Pioneering ecosystem.

Funding history:

- Seed (2022): $50M, led by a16z Bio + Health

- Series A (2023): $135M, led by ARCH

- Series B (2024): $200M, multiple strategic partners

- Late 2025: Phase 1 IND filing (B-cell lymphoma)

By Q1 2026, Kelonia had completed initial preclinical-to-clinical translation data, drawing intense pharma attention. Lilly’s acquisition completes that momentum as a preemptive absorption by a major pharma.

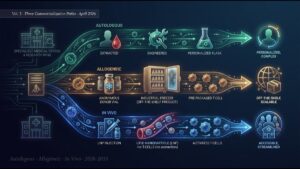

2. In Vivo CAR-T — How It Differs From Ex Vivo

To understand in vivo CAR-T, recall the conventional ex vivo workflow first.

Ex vivo CAR-T (current standard):

- Apheresis of patient T cells

- Ex vivo activation, lentiviral CAR transduction

- 2-3 weeks of expansion in GMP facility

- Lymphodepletion chemotherapy of patient

- Infusion of engineered cells

- Inpatient monitoring for CRS / ICANS

In vivo CAR-T (new approach):

- Minimal or no patient pretreatment

- CAR-encoding mRNA encapsulated in lipid nanoparticles (LNP)

- LNP surface-engineered for T-cell-selective uptake

- IV administration to patient

- Patient T cells take up LNP, express CAR within 24-48 hr

- In-body expansion of CAR-T cells, attack on tumor

- mRNA degrades within days; CAR expression is transient (days-to-weeks)

Two principle differences. First, “vector-permanent” vs “mRNA-transient” gene delivery. Second, “ex vivo” vs “in vivo” cell engineering. These differences directly drive how the three walls are softened.

3. Kelonia’s PreciseTarget LNP Technology

The reason in vivo CAR-T was long called “elegant in concept, difficult in technology” is the challenge of cell-type-selective delivery. LNPs typically traffic to the liver (the basis of approved siRNA drug Onpattro and mRNA vaccines). Targeting only T cells is a different-order challenge.

Kelonia’s PreciseTarget LNP tackles this with multiple proprietary elements:

- Surface peptide ligands: small peptide ligands that bind T-cell surface CD8 or CD3 are presented on the LNP surface, achieving T-cell-selective uptake.

- Optimized ionizable lipids: pH-dependent positive charging for endosomal escape.

- mRNA modifications: pseudouridine substitution etc. to suppress innate immune activation, maximizing CAR expression efficiency.

- Burst-kinetics control: optimized pharmacokinetics from administration to peak CAR expression to decay.

Preclinical data showed CAR expression in 20-40% of T cells in mouse and cynomolgus monkey models. While below ex vivo CAR-T cell purity (>95%), this is operationally meaningful for in vivo applications.

4. The Three Walls Kelonia Aims to Break

| Item | Ex vivo CAR-T (conventional) | In vivo CAR-T (Kelonia) |

|---|---|---|

| Manufacturing time | 2-4 weeks | Hours-1 day (LNP only) |

| Per-patient cost | $400-500K | $50-150K (estimated, declining with scale) |

| Required facility | Specialized CAR-T center | Standard oncology clinic |

| CRS / ICANS risk | 40-90% (severe 10-30%) | Unknown; preclinical trends low |

| CAR persistence | Permanent (memory T cells) | Transient (days-weeks) |

| Re-administration | Difficult | Easy (drug-like) |

“Transient CAR expression” is a double-edged sword. Long-term durable antitumor responses may be inferior to ex vivo, but if toxicity occurs, it resolves within days. The clinical design pivot is to chronic repeated dosing for cumulative effect.

5. Why Lilly Bought This

Lilly’s oncology portfolio has shifted considerably over five years. Historically anchored by Verzenio (CDK4/6 inhibitor) and Cyramza (anti-VEGFR2 antibody) — targeted small molecules and antibodies — the company is now using cash flow from Mounjaro/Zepbound’s explosive growth to fund strategic acquisitions in adjacent areas.

Three strategic intentions for Lilly:

- Insourcing a cell therapy platform: Lilly previously had no CAR-T capability and lagged competitors like Kymriah / Yescarta. After preempting the autoimmune in vivo CAR-T space via the February Orna acquisition (circular RNA + LNP), Lilly added Kelonia’s lentivirus iGPS® for oncology — assembling a two-modality, two-indication portfolio in a single year that skips 10-15 years of internal technology development.

- Acquiring an RNA / LNP / gene-delivery foundation: post-COVID vaccine era, mRNA / LNP technology is essential pharma infrastructure. Pfizer (BioNTech), Moderna (in-house), Sanofi (Translate Bio) all platformed early. Lilly was behind — but the back-to-back Orna (circular RNA + LNP) and Kelonia (lentivirus iGPS®) acquisitions assemble a distinctive RNA + gene-delivery portfolio in months rather than years.

- Multi-indication expansion: T-cell-selective LNP enables not just CAR-T but also autoimmune disease, transplant rejection, and infectious disease (HIV, chronic hepatitis) applications. Synergistic with Lilly’s autoimmune franchise (Olumiant, Taltz, Ebglyss).

6. Deal Structure — Breaking Down $7B

The “up to $7B” structure is typical of large biotech M&A:

- Upfront: $1.5-2.0B (estimated) — paid to Kelonia shareholders immediately

- Milestones: $5.0-5.5B — paid upon technical development, regulatory approval, and sales targets

This is comparable to Roche × Telavant ($7.1B, 2024), Amgen × Horizon ($28B, 2023), Pfizer × Biohaven ($11.6B, 2022). It is among the defining biotech M&A deals of the 2020s. Unusually high for a preclinical-stage company — reflecting pharma majors’ strategic determination to “lock in an in vivo CAR-T platform now.”

From a financial perspective, only the $1.5-2B upfront is guaranteed, with the remainder milestone-dependent. If Phase 1/2 succeeds and regulatory approval lands, the total could approach $7B. Kelonia founders, early VCs, and employees see strategic ROI well above 10× initial investment.

7. Immediate Impact on Competitive Players

The deal’s immediate impact across the in vivo CAR-T field:

- Valuation re-rating: Capstan, Umoja, Orna, Renagade, Sana et al. see immediate share/valuation lift; next funding rounds get easier.

- Strategic partnership demand: Other majors (Pfizer, Roche, Novartis, BMS, Merck) decide “we need a comparable platform too,” accelerating M&A, investment, and licensing negotiations with competitors.

- Talent flow: Kelonia’s founder-era staff and engineers will move into Lilly or to competitors, spreading know-how across the field.

- Regulatory dialogue acceleration: FDA / EMA frameworks for in vivo CAR-T begin to materialize as Lilly’s involvement triggers active engagement.

Volume 2 dissects these five competitors’ technical differentiation in detail.

8. Limitations and Caveats

Open issues for this deal and the field overall:

First, scarcity of Phase 1/2 clinical data. Kelonia started Phase 1 in Q1 2026; Lilly’s acquisition is preemptive, before robust efficacy/safety data. There is no guarantee in vivo CAR-T matches ex vivo on these axes.

Second, clinical implications of transient CAR expression. Targeting durable complete remission may require repeated dosing, raising LNP immunogenicity and tolerance concerns. The “single-dose long-term effect” model of ex vivo cannot be transposed directly.

Third, precision of CD8/CD3 targeting. Even with PreciseTarget LNP, T-cell selectivity is 20-40%; the remaining 60-80% reaches other tissues (liver, spleen, etc.). Off-target organ CAR expression risk is non-zero, and long-term safety data is needed.

Fourth, manufacturing scalability. mRNA / LNP gained large-scale capacity from COVID vaccines, but cell-type-selective LNP at GMP scale is a separate technical challenge requiring tech transfer time.

Summary

- 2026 saw Eli Lilly execute two consecutive in vivo CAR-T acquisitions: Feb 9 — Orna Therapeutics for up to $2.4B (circular RNA + LNP, autoimmune); Apr 21 — Kelonia Therapeutics for up to $7B (lentivirus iGPS®, oncology). The largest in vivo CAR-T M&A run to date and a definitive sign of pharma major entry.

- Kelonia’s PreciseTarget LNP technology delivers CAR mRNA to T cells in the patient’s body, potentially softening conventional CAR-T’s three walls (manufacturing time, cost, toxicity) simultaneously.

- Lilly’s strategic intent: insourcing cell-therapy platform (two-modality Orna + Kelonia), RNA / LNP / gene-delivery foundation, autoimmune + oncology multi-indication expansion potential.

- $7B structure: upfront $1.5-2B + milestones $5-5.5B. Among the defining biotech M&A deals of the 2020s.

- Field-level impact: re-rating of valuations, accelerating M&A across competitors, talent flow, regulatory dialogue acceleration.

- Open issues: limited clinical data, transient CAR expression’s clinical model redesign, off-target organ CAR expression risk, GMP scale-up hurdles.

My Thoughts and Outlook

The deal’s structural significance is capturing the moment “mRNA / LNP technology extends from infectious-disease vaccines to cell therapy.” The Pfizer-BioNTech / Moderna platform proven through COVID is no longer a niche technology — it is the foundational platform for gene therapy and cell therapy. Lilly is using this to leap from the loser side of the past decade’s gene-therapy race (AAV, lentivirus-centered) to the front of the next-generation race.

Three structural implications for the global research and industry community. First, mRNA/LNP platforms become the foundational pharma infrastructure for the 2020s-2030s. Any major pharma without an internal mRNA/LNP capability is now strategically disadvantaged. M&A waves comparable to AAV gene therapy will continue. Second, the boundary between “drug” and “cell therapy” blurs. In vivo CAR-T is administered like a drug but acts like a cell therapy. Regulatory frameworks (FDA’s CBER vs CDER), reimbursement codes, and manufacturing supply chains all need to evolve. The first FDA-approved in vivo CAR-T product (likely 2028-2030) will define the new paradigm. Third, cell-therapy access is undergoing an “accessibility revolution.” Ex vivo CAR-T was confined to specialized centers in wealthy countries. In vivo CAR-T can be administered in standard oncology clinics. If patient-unit cost reaches $50-150K, hundreds of thousands of additional patients globally become accessible — a dramatic medical-economic shift.

2026 is the year AI is rapidly commoditizing knowledge work. In vivo CAR-T sits squarely in the “AI cannot replace” zone — requiring physical molecular engineering (LNP design), regulatory dialogue with body-based clinical evidence, and manufacturing infrastructure. This is precisely the type of frontier where a single acquisition can reshape an entire industry.

Coming Next

Volume 2 dissects the technical differentiation of the in vivo CAR-T main players: Capstan Therapeutics (AbbVie subsidiary, $2.1B, June 2025), Umoja Biopharma, Renagade Therapeutics, and Sana Biotechnology, alongside the repositioned Orna Therapeutics as a Lilly subsidiary. We compare each company’s LNP platform choice, CAR target, indication focus, clinical stage, and strategic partnerships — and project the field reshuffling under the AbbVie-Capstan vs Lilly-(Orna+Kelonia) two-camp structure.

Edited by the Morningglorysciences team.

Comments