Key Takeaways

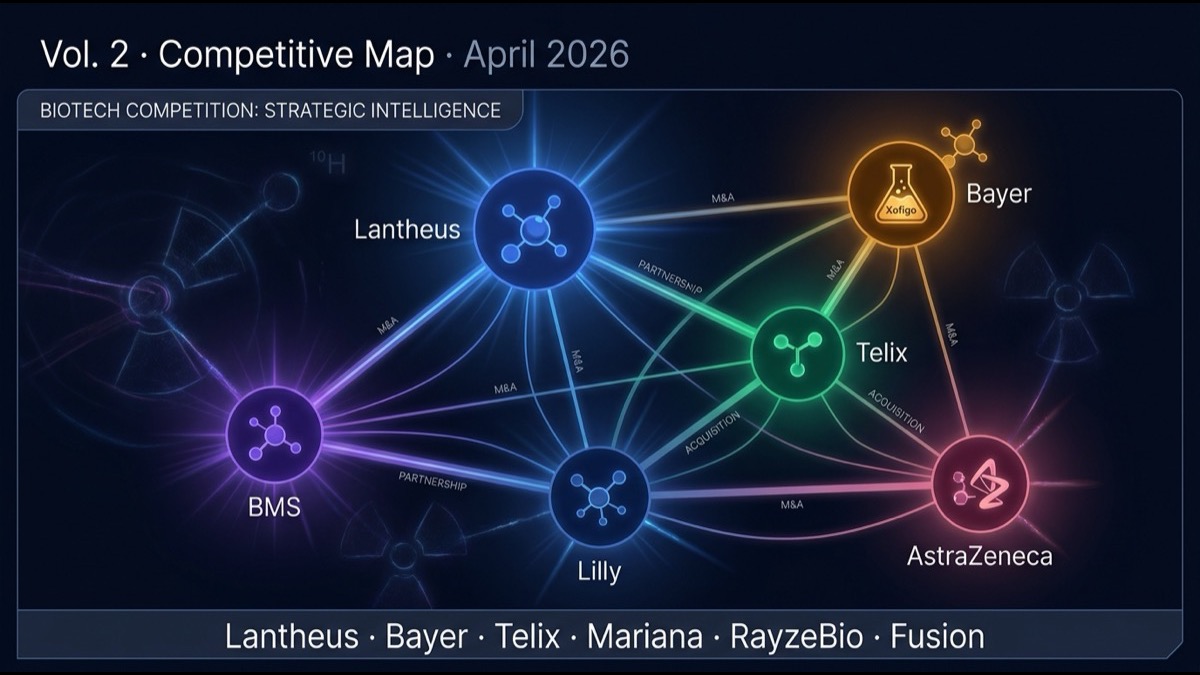

- Following Volume 1’s coverage of Novartis leadership, this article dissects major nuclear medicine competitors: Lantheus (diagnostic + treatment), Bayer (Xofigo veteran, α-emitter next-gen), Telix (Australia-origin, PSMA diagnostic + FAP treatment), Lilly × Mariana / BMS × RayzeBio (major newcomers), and emerging biotechs (Aktis, Convergent, Perspective, Fusion, etc.)

- Five differentiation axes: (1) diagnostic vs treatment focus, (2) target molecules (PSMA, SSTR, FAP, GD2, HER2, αvβ6), (3) isotope choice (¹⁷⁷Lu vs Ac-225 vs Pb-212), (4) manufacturing infrastructure, (5) strategic partnerships.

- The industry is converging into a “vertically integrated big pharma vs specialized biotech” bipolar structure. Novartis, BMS, Lilly, Bayer pursue vertical integration; Lantheus, Telix start from diagnostics expanding to treatment; emerging biotechs survive via specific target / isotope niches.

- Expect a second wave of large M&A in the next 3-5 years. Targets: Aktis Oncology (FAP), Convergent Therapeutics (PSMA Ac-225), Perspective Therapeutics (Pb-212), Fusion Pharmaceuticals (AstraZeneca acquired for $2B in 2024), Telix (independent vs strategic acquisition).

Introduction — “In the Shadow of Leader Novartis”

Volume 1 covered Novartis’s Pluvicto / Lutathera success and Vertical Integration strategy. But nuclear medicine is not a Novartis monopoly — multiple competitors run in parallel. This article compares each across five axes — diagnostic vs treatment, target molecule, isotope, manufacturing infrastructure, partnerships — and describes industry reshuffling scenarios.

Main Body

1. Lantheus Holdings — Diagnostic Nuclear Medicine Champion

Headquarters: Massachusetts. NASDAQ: LNTH. 2025 revenue: ~$1.5B (estimated).

- PYLARIFY (¹⁸F-PSMA-1007): standard prostate cancer PET diagnostic. Over 1M tests/year in the US.

- DEFINITY: cardiac echo ultrasound contrast, stable cardiovascular cash flow.

- RELISTOR: opioid-induced constipation drug.

- 2024 strategic expansion announcement into treatment: in-house Pb-212 / Ac-225 platform development.

Strengths: dominance in diagnostic market, manufacturing-distribution network, US footprint. Weaknesses: lagging clinical stage in treatment.

2. Bayer — Xofigo Veteran, Entering the α Era

Bayer secured FDA approval of Xofigo (²²³Ra) in 2013 — the α-emitter therapy pioneer for prostate cancer bone metastasis.

- ²²³Ra Xofigo: clinical establishment of α therapy (ALSYMPCA trial, NEJM 2013).

- Next-generation pipeline: ²²⁵Ac PSMA-617 (Bayer strategic partnership), actin receptor targets.

- Manufacturing infrastructure: European Bayer Buenos Aires, Berkeley RI manufacturing.

Strengths: α therapy clinical experience. Weaknesses: slower new product development pace vs Pluvicto.

3. Telix Pharmaceuticals — From PSMA Diagnostic to Treatment

Australia-origin, ASX/NASDAQ: TLX. 2025 revenue: ~$500M.

- Illuccix (⁶⁸Ga-PSMA-11): prostate cancer PSMA-PET diagnostic, direct PYLARIFY competitor.

- Treatment pipeline: TLX591 (¹⁷⁷Lu-PSMA-I&T) for prostate, TLX250 (CAIX target, RCC).

- Geographic expansion: Australia, US, EU, Asia (including Japan).

Strengths: natural diagnostic-to-treatment expansion path, global multi-region. Weaknesses: smaller scale than Novartis / Lantheus.

4. Eli Lilly × Mariana Oncology — Betting on FAP α Therapy

After losing the Point Biopharma bid in 2023, Lilly acquired Mariana Oncology for $1.0B in 2024. Mariana is a Boston biotech developing FAP (fibroblast activation protein) targeted Ac-225 therapy.

- FAP target: expressed on tumor-associated fibroblasts, applicable to solid tumors broadly (PSMA limited to prostate, SSTR to NET, but FAP is a generalist target).

- ²²⁵Ac α-emitter: more cytotoxic than β-emitter, with shorter range limiting normal-tissue impact.

- Lilly’s massive cash flow from Mounjaro / Zepbound enables strategic acceleration.

Strengths: FAP generalist target market potential, parent company financial firepower. Weaknesses: Phase 1 clinical stage; full establishment 2-3 years away.

5. Bristol Myers Squibb × RayzeBio — Major Entry via Mega-Acquisition

BMS acquired RayzeBio for $4.1B in December 2023. RayzeBio is a San Diego biotech with an ²²⁵Ac core platform.

- RYZ101 (²²⁵Ac-DOTATATE): NET treatment, alternative to Lutathera (¹⁷⁷Lu).

- ²²⁵Ac platform: extension to multiple targets / indications.

- BMS oncology global commercial capabilities (Opdivo, Yervoy).

Strengths: BMS oncology execution, multi-Ac-225 pipeline scale. Weaknesses: strategic priority within BMS (internal competition with Opdivo-led oncology).

6. AstraZeneca × Fusion Pharmaceuticals — Next-Gen Canadian Acquisition

AstraZeneca acquired Fusion Pharmaceuticals for $2B in April 2024. Fusion (Canada) develops ²²⁵Ac PSMA / FAP therapy.

- FPI-2059 (²²⁵Ac-IPN-1072, NTSR1 target): pancreatic, colorectal cancers.

- FPI-2068 (²²⁵Ac-PSMA): prostate cancer, Pluvicto competitor.

- AstraZeneca oncology synergy with Lynparza, Imfinzi.

7. Emerging Specialists

Independent startups potential targets for large M&A:

- Aktis Oncology: Boston, FAP-targeting Ac-225/Pb-212, Phase 1 progressing. Acquisition candidates: Novartis, BMS, Pfizer.

- Convergent Therapeutics: PSMA Ac-225, late Phase 2.

- Perspective Therapeutics (NASDAQ: CATX): ²¹²Pb core platform, public.

- Curasight: Denmark, uPAR / FAP α therapy.

- Clarity Pharmaceuticals (ASX: CU6): Australia, Cu-64 / Cu-67 pair “theranostic” approach.

- POINT Biopharma successor spinout teams: multiple small ventures.

8. Industry Reshuffling Scenarios

Three-to-five-year forecast:

Scenario 1: Aktis Oncology acquired (high probability). FAP generalist target attracts Pfizer / Roche / Merck strategic interest. $2-4B range.

Scenario 2: Telix continues independent or acquired by AstraZeneca / Roche (medium). Diagnostic + treatment pipeline draws major attention.

Scenario 3: Lantheus large M&A in Pb-212/Ac-225 treatment (medium). Diagnostic cash flow channeled into treatment development.

Scenario 4: Multiple small biotech serial acquisitions (high). Convergent, Perspective, Curasight etc. progressively become acquisition targets.

Summary

- Nuclear medicine field has a bipolar competitive structure with Novartis at the apex and Lantheus, Bayer, Telix, Lilly × Mariana, BMS × RayzeBio, AZ × Fusion as major players.

- Differentiation axes: diagnostic vs treatment, target molecules (PSMA, SSTR, FAP, GD2, etc.), isotopes (¹⁷⁷Lu vs Ac-225 vs Pb-212), manufacturing infrastructure, strategic partnerships.

- Emerging specialists: Aktis, Convergent, Perspective, Curasight, Clarity as large M&A candidates.

- Reshuffling forecast: Aktis acquired (high), Telix strategic transition (medium), Lantheus treatment-area M&A (medium), small biotech serial acquisitions (high).

My Thoughts and Outlook

Nuclear medicine competitive structure represents a rare “manufacturing × pharmaceutical hybrid industry” in pharma. As Volume 1 highlighted, Vertical Integration’s importance differs from typical cancer therapy competitive dynamics — single-molecule patent monopoly is not enough; rather, ecosystem control over isotope supply networks, GMP manufacturing capabilities, and regulatory navigation is decisive.

Three structural implications for the global ecosystem. First, isotope production becomes strategic infrastructure. Beyond traditional reactor sites (Belgium IRE, Netherlands NRG, Russia Rosatom), commercial-scale ¹⁷⁷Lu and Ac-225 production facilities are being built in the US, EU, Asia. Country-level isotope production investment is becoming as important as semiconductor fabrication for medical sovereignty. Second, the boundary between “subcategories of biopharmaceuticals” is dissolving. Nuclear medicine, mRNA-LNP gene therapy, and CAR-T cell therapy increasingly resemble each other in requiring vertically integrated, time-critical, highly engineered platforms. Third, regulatory convergence is critical. FDA RPP review pathway, EMA ATMP designation, PMDA regenerative medicine framework, and emerging APAC pathways — alignment determines which markets see new nuclear medicines first.

2026 is the year AI is rapidly commoditizing knowledge work. Nuclear medicine sits squarely in the “AI cannot replace” zone. Volume 3 (final) will explore α-emitter therapy (Ac-225, Pb-212) clinical pipelines and the next-generation target landscape.

Coming Next

Volume 3 (final) dissects α-emitter therapy (Ac-225, Pb-212) clinical pipelines. Why α is more promising than β, current trial stages, next targets (FAP, GD2, HER2, αvβ6), and the next decade’s direction for nuclear medicine.

Edited by the Morningglorysciences team.

Comments