Key Takeaways

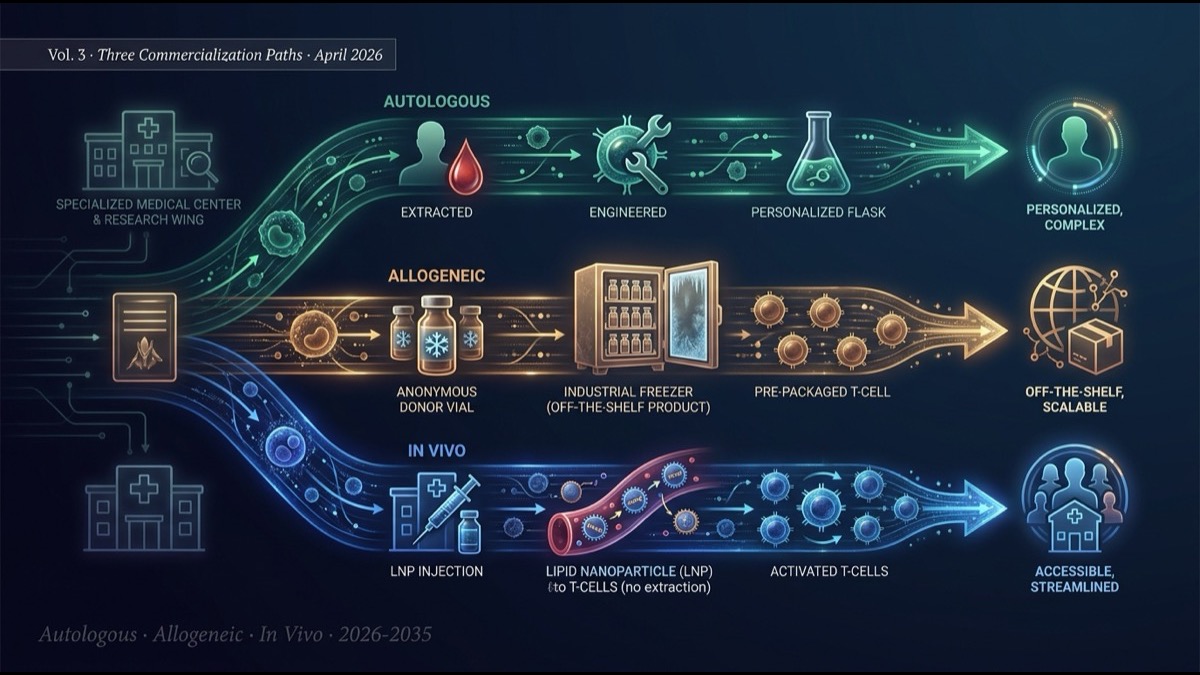

- The series finale compares the three commercialization paths driving CAR-T’s evolution: autologous, allogeneic, and in vivo. Each path embodies distinct technical, economic, and regulatory “design philosophies” — and they will likely coexist in the market rather than displace one another.

- Autologous CAR-T (Kymriah, Yescarta, Carvykti, etc.) has been the standard since 2017. With 5+ years of market data and the most mature long-term complete remission evidence, it remains the gold standard despite the structural constraints of $400-500K per patient cost, 2-4 week manufacturing time, and specialized-center delivery.

- Allogeneic CAR-T (Allogene, Caribou, Wugen, Atara, etc.) takes the “off-the-shelf cell therapy” approach: master cells from healthy donors, mass-produced. Manufacturing time near-zero, cost a fraction of autologous, GVHD risk controlled with TALEN/CRISPR editing — but HvG (host-vs-graft) rejection shortens persistence and reduces long-term response rates compared to autologous.

- In vivo CAR-T (covered in Vol. 1-2) is the “ultimate form” — patient cells are not extracted at all. LNP-mRNA, LV-pseudotyped, and other delivery technologies enable standard clinic delivery. It can soften ex vivo’s three walls simultaneously, but Phase 1 data through 2026-27 will determine its trajectory.

- The three paths are settling into structural role differentiation. Autologous: refractory and rare disease, long-term complete remission. Allogeneic: emergency access, short-term response, cost sensitivity. In vivo: chronic autoimmune, repeated dosing, global accessibility. Over the next decade, these three paths will complement rather than substitute one another, with optimization by indication.

Introduction — Not “the Strongest CAR-T,” but Three Design Philosophies

Volumes 1 and 2 covered the latest in vivo CAR-T developments (Lilly × Kelonia $7B, the five-company landscape). The finale broadens the lens to the entire CAR-T industry — autologous, allogeneic, in vivo — for structural comparison.

The industry often debates “which is the strongest.” This is the wrong question. Each of the three paths embodies a distinct design philosophy responding to distinct clinical needs. They are complementary, not mutually exclusive. This article maps the three paths across seven axes — per-patient cost, manufacturing time, efficacy, toxicity profile, regulatory environment, market scale, and indication fit — and projects the next decade of CAR-T industry geography.

Main Body

1. Autologous CAR-T — Five-Plus Years of Market Track Record

Autologous CAR-T involves extracting patient T cells, ex vivo gene editing, expansion, and reinfusion. Since FDA approval of Kymriah (Novartis) and Yescarta (Gilead) in 2017, the field has accumulated about eight years of market experience.

Key approved products:

- Kymriah (tisagenlecleucel): CD19 CAR-T, acute B-cell leukemia, large B-cell lymphoma

- Yescarta (axicabtagene ciloleucel): CD19 CAR-T, large B-cell lymphoma, follicular lymphoma

- Tecartus (brexucabtagene autoleucel): CD19 CAR-T, mantle cell lymphoma, ALL

- Breyanzi (lisocabtagene maraleucel): CD19 CAR-T, large B-cell lymphoma

- Abecma (idecabtagene vicleucel): BCMA CAR-T, multiple myeloma

- Carvykti (ciltacabtagene autoleucel): BCMA CAR-T, multiple myeloma

Combined market size as of 2025 is roughly $5.0B/year. Carvykti has grown 2× year-over-year, driving market expansion through earlier-line multiple myeloma penetration (post Phase 3 CARTITUDE-4 positive results).

The long-term efficacy data (5-7 year follow-up) for autologous CAR-T continues to mature. Approximately 50-60% of pediatric ALL patients achieve long-term complete remission, and over 40% of large B-cell lymphoma patients maintain complete response for 3+ years. These figures are unattainable with standard chemotherapy. This is autologous CAR-T’s long-term durability advantage over the other two paths.

2. Allogeneic CAR-T — The Off-the-Shelf Vision and Reality

Allogeneic CAR-T mass-produces healthy-donor T cells as master cells, dosing multiple patients. The promise of “off-the-shelf cell therapy” — keeping product frozen, thawing on demand — could dramatically reduce manufacturing time and per-patient cost.

Key players:

- Allogene Therapeutics (NASDAQ: ALLO): CD19 and BCMA TALEN-edited T cell therapies. ALLO-647 (anti-CD52) for “Selective Lymphodepletion” protocol.

- Caribou Biosciences (NASDAQ: CRBU): CRISPR-Cas12a + Cas9 multi-edited advanced allogeneic T cell therapies.

- Wugen: iPSC-derived NK / T cell therapies.

- Atara Biotherapeutics (NASDAQ: ATRA): EBV-specific T cell therapies.

- Cellectis (NASDAQ: CLLS): TALEN technology platform, Allogene-partnered.

Two technical challenges for allogeneic CAR-T:

- GVHD (graft-versus-host disease): donor T cells attack patient tissues. Resolved by TALEN/CRISPR editing of TCR genes to delete T-cell receptors.

- HvG (host-versus-graft) rejection: patient immune system rejects foreign T cells. Addressed via CD52, HLA-class I editing and chemotherapy-based immunosuppression. Persistence is shorter than autologous (weeks-to-months); long-term response rates lag autologous.

Market reality: as of May 2026, no FDA-approved allogeneic CAR-T product exists. Allogene’s ALLO-501 in late-phase trials for relapsed/refractory B-cell lymphoma; Caribou’s CB-010 in late phase. First regulatory approvals are expected in 2026-27, but compared to autologous efficacy, “second-best” perception may persist initially.

3. In Vivo CAR-T — The “Ultimate Form” Covered in Vols. 1-2

In vivo CAR-T extracts no patient cells, instead using mRNA, viral vectors, etc. delivered directly to the patient to generate CAR-T inside the body — the ultimate simplification. Volume 1 covered Lilly’s two-step 2026 acquisition (Orna + Kelonia); Volume 2 dissected the main players (AbbVie-owned Capstan, Lilly-owned Orna, and the independent remainders Umoja, Renagade, Sana).

Status as of May 2026: zero FDA-approved products, all companies in Phase 1. Commercialization is projected for 2028-30. But Lilly’s back-to-back acquisitions of Orna (Feb 2026, $2.4B) and Kelonia (Apr 2026, $7B) demonstrate that major pharma’s strategic investment has fully begun, and technical-financial momentum is strong.

4. Three-Path Structural Comparison

| Axis | Autologous | Allogeneic | In vivo |

|---|---|---|---|

| Manufacturing time | 2-4 weeks | Pre-manufactured (immediate) | Hours-1 day (LNP) |

| Per-patient cost | $400-500K | $100-200K | $50-150K (estimated) |

| Required facility | Specialized center | Specialized center | Standard clinic |

| Long-term durability | High (5-yr data) | Medium (HvG rejection) | Unknown |

| Toxicity management | Inpatient/ICU | Inpatient | Outpatient possible |

| Repeated dosing | Difficult | Possible | Easy |

| Indication fit | Refractory, rare, young | Emergency access, cost-sensitive | Chronic autoimmune, global |

| Commercial status | 6 approved, $5.0B/yr | Phase 2-3, near approval | Phase 1, 2028-30 approval |

| Regulatory path | BLA | BLA | BLA + protocol reform |

5. Optimal-Path Map by Indication

Optimal path varies by indication. Mapping clinical needs to technical profiles:

Autologous CAR-T optimal areas

- Refractory B-cell malignancies (DLBCL 3rd-line+, relapsed ALL): long-term complete remission essential, treatment efficacy outweighs manufacturing time.

- Multiple myeloma (relapsed/refractory): BCMA CAR-T with mature 5-7 year follow-up data.

- Pediatric and young adult ALL: chemo bridge during manufacturing, long-term cure goal.

Allogeneic CAR-T optimal areas

- Refractory acute leukemia requiring emergency access: 2-4 week autologous manufacturing impossible.

- Emerging markets and regional medical centers: cannot meet specialized-center requirements for autologous.

- Maintenance and repeated dosing post-initial therapy: prioritize repeatability over long-term durability.

- Solid tumors (multi-NK/T cell injection for infiltration promotion): multi-dose model rather than single-dose.

In vivo CAR-T optimal areas

- Chronic autoimmune disease (lupus, RA, MS, SLE): repeated dosing model fits perfectly, outpatient management.

- Global accessibility-priority indications: low cost + standard clinic delivery reaches global oncology infrastructure.

- Transplant rejection / GVHD: T-cell modulation for immune control.

- Chronic viral infections (HIV, chronic hepatitis): cell-therapy curative approach.

6. Regulatory Environment — FDA, EMA, and APAC

CAR-T commercialization is inseparable from regulation. The three paths require different regulatory responses.

FDA: autologous and allogeneic both via CBER (Center for Biologics Evaluation and Research) BLA pathway. In vivo CAR-T sits between “mRNA therapy” and “cell therapy,” potentially requiring a new regulatory category. In April 2026, FDA initiated industry advisory meetings on in vivo CAR-T to develop the regulatory framework.

EMA: Europe manages autologous and allogeneic under the ATMP (Advanced Therapy Medicinal Products) framework. In vivo CAR-T can be filed under ATMP “gene therapy” subcategory.

APAC regulators: regional fragmentation persists. Singapore HSA, South Korea MFDS, and India CDSCO are advancing different pathways. Conditional approval pathways and accelerated review programs vary; this creates strategic optionality for first-in-region launches.

7. Market Scale and Future Projections

| Year | Autologous | Allogeneic | In vivo | Total |

|---|---|---|---|---|

| 2025 | $5.0B | $0.1B | $0 | $5.1B |

| 2028 | $8.0B | $1.5B | $0.5B | $10.0B |

| 2030 | $10B | $3.5B | $3.0B | $16.5B |

| 2035 | $12B | $8B | $15B | $35B |

Notably, in vivo CAR-T may overtake the other two paths in 2030-35. This is the “accessibility revolution” effect — when in vivo CAR-T becomes available at standard clinics, patients globally previously excluded from CAR-T access become treatable.

8. Limitations and Caveats

Caveats for this structural comparison:

First, market projection uncertainty. In vivo CAR-T Phase 1/2 data through 2026-28 will determine long-term durability, toxicity profile, and repeated-dosing clinical validity. These results may shift projections by ±50%.

Second, fluidity of optimal-path mapping by indication. Technical improvements in each path (autologous manufacturing shortening, allogeneic HvG suppression improvement, in vivo persistence enhancement) will continuously alter optimal allocation.

Third, geographic diversity of regulatory and reimbursement structures. US, EU, Japan, and emerging markets (China, India, Brazil) differ significantly. Global commercialization strategy varies substantially by path.

Summary

- The three CAR-T commercialization paths — autologous, allogeneic, in vivo — embody distinct technical, economic, and regulatory design philosophies and will coexist complementarily.

- Autologous: 5+ years of market evidence, 6 approved products, $5.0B/yr scale. Long-term durability advantage. Structural constraints (cost, manufacturing time, specialized centers) gradually improving.

- Allogeneic: “off-the-shelf” vision, near-zero manufacturing time, fraction-of-autologous cost. GVHD controlled by TALEN/CRISPR editing; HvG rejection limits long-term durability. First FDA approval expected 2026-27.

- In vivo: “ultimate form” simplicity, standard clinic delivery. Lilly × Kelonia $7B accelerates the field. Phase 1 data leaves trajectory uncertain, but first approval expected 2028-30.

- Optimal path by indication: autologous = refractory/rare/young; allogeneic = emergency access/cost-sensitive; in vivo = chronic autoimmune/global accessibility.

- Market projection: 2030 total $16.5B, 2035 $35B. In vivo’s late-decade growth produces a balanced three-path market.

Series Synthesis

Across the three-volume series “The In Vivo CAR-T Revolution,” we have mapped the technical, competitive, and industrial landscape of in vivo CAR-T from Lilly’s two-step 2026 M&A — Orna (Feb 9, $2.4B) and Kelonia (Apr 21, $7B) — as the inflection point.

Volume 1: significance of Lilly’s two-step Orna + Kelonia acquisitions and strategic intent. The PreciseTarget LNP technology core. Why in vivo CAR-T can soften ex vivo’s three walls simultaneously.

Volume 2: in vivo CAR-T main players (AbbVie-owned Capstan, Lilly-owned Orna, and the independent remainders Umoja, Renagade, Sana) — technical differentiation axes and industry reshuffling scenarios.

Volume 3 (this article): integrated comparison of autologous, allogeneic, and in vivo. Optimal-path mapping by indication and market projections.

The deepest structural change visible across the series is that “the CAR-T industry is moving from single-modality competition to a mature stage of three-path coexistence with indication-by-indication optimization.” This is more sophisticated industry architecture than the simple “autologous-only” era of the 2010s.

My Thoughts and Outlook

The series synthesis points to the largest insight: “CAR-T is no longer a single drug category but a comprehensive cell-therapy / gene-therapy platform.” Autologous, allogeneic, and in vivo each embody distinct engineering design philosophies, with clinical indications matching each path’s strengths emerging clearly. Over the next decade, these three paths will coexist complementarily, with optimal selection driven by individual patient clinical needs and indication characteristics.

Three structural implications for the global ecosystem. First, “drug” and “cell therapy” boundaries continue to blur. In vivo CAR-T is administered like a drug but acts like cell therapy. Regulatory (FDA CBER vs CDER), reimbursement codes, and manufacturing infrastructure must evolve. The first FDA-approved in vivo CAR-T (likely 2028-30) defines the new paradigm. Second, autoimmune disease becomes a major battleground. Lupus, RA, MS — these chronic diseases match in vivo CAR-T’s repeated-dosing model perfectly. The autoimmune CAR-T market may exceed the oncology CAR-T market by 2030. Third, the accessibility revolution reshapes global oncology economics. When in vivo CAR-T reaches $50-150K per patient at standard clinics, hundreds of thousands of additional patients globally become treatable. This is medical-economic transformation comparable to vaccine globalization.

2026 is the year AI is rapidly commoditizing knowledge work. CAR-T sits in the “AI cannot replace” zone — physical molecular engineering, regulatory navigation, manufacturing infrastructure, clinical delivery. This series has spotlighted three paths that AI alone cannot create. I hope to continue sharing this CAR-T evolution with readers who completed the series.

Edited by the Morningglorysciences team.

Comments