Key Takeaways

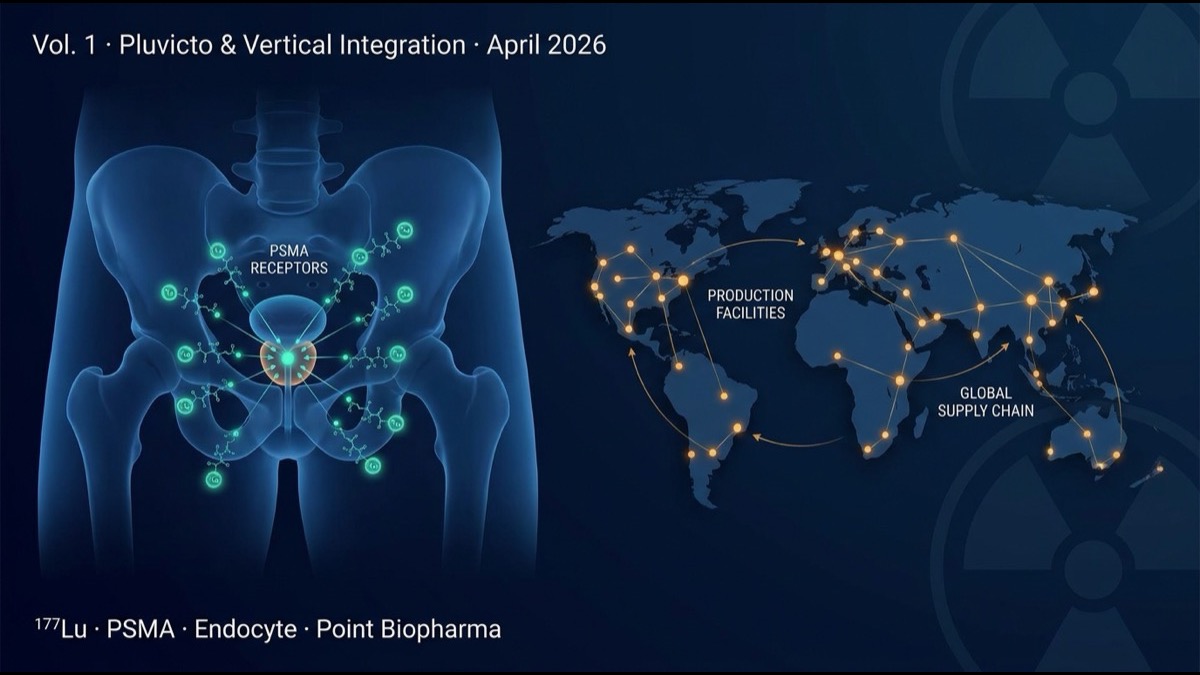

- Novartis’s Pluvicto ([¹⁷⁷Lu]Lu-PSMA-617) was approved by FDA in 2022 and has grown to over $1B in annual sales as a new axis in metastatic castration-resistant prostate cancer (mCRPC) treatment. Together with their Lutathera ([¹⁷⁷Lu]Lu-DOTATATE) for neuroendocrine tumors, they have catalyzed nuclear medicine’s transition from “niche” to “mainstream.”

- The April 2026 BioSpace industry analysis emphasizes that “Vertical Integration” is essential for sustaining nuclear medicine’s market growth. Without controlling the full chain from radioisotope production through drug synthesis, distribution, and clinical delivery, the structural barriers from short isotope half-lives (hours to days) and specialized facility requirements cannot be overcome.

- Novartis acquired Endocyte for $2.1B in 2018 (Pluvicto), Point Biopharma for $1.4B in 2023 (Pb-212, Ac-225 next-generation pipeline), and expanded its isotope production network to 14 sites globally. The “product to patient” strategy is taking shape.

- Competitors are following: Lantheus, Bayer, Telix, Eli Lilly (acquired Mariana Oncology for $1.0B in 2024 after losing the Point Biopharma bid), Bristol Myers Squibb ($4.1B for RayzeBio in 2023). The next 5 years will reshape the nuclear medicine industry.

Introduction — From “Niche Specialty” to “Main Stage”

Nuclear medicine (radiopharmaceutical therapy, targeted radionuclide therapy) was viewed for 30 years as “a specialty within specialties” — provided only at a handful of major academic medical centers, a “specialized treatment” administering radioisotopes to patients. Market size and academic attention were both limited.

That changed with Novartis’s clinical and commercial success of Pluvicto and Lutathera. Pluvicto received FDA approval in March 2022, achieved survival prolongation in mCRPC, and grew to over $1B in annual revenue. Lutathera was approved in 2018 and became part of standard NET therapy. Combined annual revenue is approximately $3B in 2025.

The April 2026 BioSpace industry analysis pointed to Vertical Integration as the key structural growth driver for the nuclear medicine market. This article explores Pluvicto’s success, the necessity of Vertical Integration, and the direction of industry reshuffling.

Main Body

1. How Pluvicto Changed Prostate Cancer Treatment

Pluvicto ([¹⁷⁷Lu]Lu-PSMA-617) targets prostate-specific membrane antigen (PSMA). The structure binds a small molecule (PSMA-617) to β-emitting lutetium-177 (¹⁷⁷Lu, half-life 6.7 days). It selectively recognizes PSMA highly expressed on prostate cancer cells, internalizes, and delivers β-radiation to induce cell death from inside.

Phase 3 VISION trial (NEJM 2021) compared standard of care + Pluvicto vs standard of care alone in mCRPC:

- Radiographic progression-free survival (rPFS): 8.7 vs 3.4 months (HR 0.40, P<0.001)

- Overall survival (OS): 15.3 vs 11.3 months (HR 0.62, P<0.001)

- Main side effects: reversible bone marrow suppression, dry mouth (PSMA is also expressed in salivary glands)

This was significant survival prolongation in standard-treatment-failed prostate cancer patients — clinical value of immense importance. With approximately 500,000 mCRPC patients globally per year, Pluvicto established itself in 3rd-4th line of standard treatment.

2. Lutathera — Driving Nuclear Medicine’s Clinical Establishment

Before Pluvicto, Novartis already had Lutathera ([¹⁷⁷Lu]Lu-DOTATATE), approved in 2018 for NET (neuroendocrine tumors). Lutathera targets somatostatin receptor (SSTR) and is widely used in gastrointestinal/pancreatic NET.

Lutathera’s clinical establishment (NETTER-1 trial, NEJM 2017) paved the regulatory and market acceptance pathway for Pluvicto. FDA, EMA, PMDA established safety profiles, dosimetry, and manufacturing standards for [¹⁷⁷Lu] therapy through Lutathera, which prepared the way for Pluvicto.

3. Vertical Integration — Why It’s Essential in Nuclear Medicine

Nuclear medicine differs decisively from other pharmaceuticals due to radioisotope half-life and physical handling.

| Isotope | Half-life | Radiation | Use |

|---|---|---|---|

| ¹⁷⁷Lu | 6.7 days | β | Pluvicto, Lutathera |

| ²²⁵Ac | 9.9 days | α | Next-gen PSMA, FAP, GD2 |

| ²¹²Pb | 10.6 hours | β (α decay) | Point Biopharma core |

| ⁶⁸Ga | 67.7 min | positron | Diagnostic (PET) |

| ¹⁸F | 110 min | positron | Diagnostic (PET) |

| ⁹⁹ᵐTc | 6.0 hours | γ | Diagnostic (SPECT) |

These short half-lives impose entirely different commercial design requirements vs typical pharmaceuticals:

- Manufacturing-to-administration must complete within hours to days.

- A global production-distribution network is required.

- Specialized facilities (radiation control, radioactive waste, dedicated infusion rooms) are needed.

- Specialized personnel (nuclear medicine physicians, radiologic technologists, RI-handling pharmacists)

These structural requirements make “product-to-patient” Vertical Integration a decisive competitive advantage. Novartis has expanded Pluvicto manufacturing to 14 sites globally, covering major US/EU/Japan/Asia markets — a barrier to entry competitors cannot easily overcome.

4. Novartis’s Strategic Acquisitions — Endocyte and Point Biopharma

Novartis built its nuclear medicine platform via two strategic acquisitions.

2018 Endocyte ($2.1B): At the time, Endocyte was a small biotech running the Phase 3 VISION trial of Pluvicto (then ¹⁷⁷Lu-PSMA-617). Novartis acquired this clinical asset and brought Pluvicto to commercial trajectory.

2023 Point Biopharma ($1.4B): Point owned platforms for next-generation α-emitting and short-half-life β-emitting isotopes (Pb-212, Ac-225). Novartis thereby gained the foundation to extend beyond Pluvicto (¹⁷⁷Lu) into the “α era.”

Novartis additionally invested in isotope production facilities in Italy, US, Japan, France etc. Securing in-house ¹⁷⁷Lu supply resolved Pluvicto’s supply bottleneck.

5. Competitor Response — Lantheus, Bayer, Lilly, BMS

Following Novartis’s success, other major pharma and specialty companies have accelerated nuclear medicine investment:

- Lantheus (NASDAQ: LNTH): dominant in diagnostic nuclear medicine. PYLARIFY (PSMA-PET diagnostic) controls prostate cancer diagnosis market. Treatment expansion underway.

- Bayer: Xofigo (Ra-223) pioneered prostate bone metastasis treatment. Internal next-generation isotope (Ac-225) pipeline development.

- Eli Lilly: After losing the Point Biopharma bid in 2023, acquired Mariana Oncology for $1.0B in 2024. Gained Ac-225 / FAP-targeted nuclear medicine.

- Bristol Myers Squibb: Acquired RayzeBio for $4.1B in 2023, gaining Ac-225 core platform and rapidly establishing nuclear medicine business.

- Telix Pharmaceuticals (ASX/NASDAQ: TLX): Australian-origin, Illuccix (PSMA-PET diagnostic) entered diagnostic market. Treatment pipeline expanding.

The combined size of these large M&A deals (over $10B total) reflects pharma majors’ strategic commitment to nuclear medicine.

6. Market Size and Future Projections

Integrating various market research forecasts (treatment-only RI; excluding diagnostics):

- 2025: ~$6B

- 2030: $15-20B (20% annual growth)

- 2035: $30-40B

Growth drivers:

- Pluvicto expansion in prostate cancer (later → earlier lines)

- Lutathera indication expansion to other NETs

- Next-generation nuclear medicines targeting PSMA, FAP, GD2, SSTR, etc.

- α-emitter (Ac-225, Pb-212) clinical establishment

7. Regulatory Environment and Clinical Implementation Challenges

Multiple regulatory and operational challenges in nuclear medicine clinical implementation:

First, facility requirements. FDA, EMA, PMDA require strict facility certification. Establishing a “radiopharmaceutical-handling facility” can take 1-2 years.

Second, dosimetry and individual optimization. Pluvicto’s standard dose is fixed, but real-world clinical practice debates patient-specific optimization based on renal function, marrow function, and tumor burden.

Third, radioactive waste management. Patient urine, stool, blood, medical waste post-administration are all regulated.

Fourth, combination therapy. Multiple trials are ongoing for ICI combinations, sequencing with chemotherapy / hormone therapy, etc.

8. Limitations and Caveats

First, manufacturing bottlenecks. Global ¹⁷⁷Lu supply is limited and may not keep up with rapidly growing Pluvicto demand. Novartis is investing in expansion, but industry-wide supply capacity remains a 3-5 year challenge.

Second, long-term safety. Secondary malignancy risk after ¹⁷⁷Lu therapy requires long-term follow-up.

Third, cost and reimbursement. A standard Pluvicto course costs over $200K. Reimbursement structures vary across US, EU, Japan.

Summary

- Novartis’s Pluvicto (mCRPC) and Lutathera (NET) clinical and commercial success has moved nuclear medicine from “niche” to “mainstream.”

- Vertical Integration (production, drug synthesis, distribution, clinical delivery in one chain) is decisive competitive advantage due to short half-lives and specialized facility requirements.

- Novartis strategy: Endocyte ($2.1B), Point Biopharma ($1.4B), 14-site isotope production network — “product to patient” control.

- Competitors following: Lilly × Mariana ($1.0B), BMS × RayzeBio ($4.1B), Bayer, Lantheus, Telix strategic investments.

- Market: $6B (2025) → $15-20B (2030) → $30-40B (2035) at 20% annual growth.

- Limitations: manufacturing bottleneck, long-term safety, cost/reimbursement, facility requirements.

My Thoughts and Outlook

The structural changes in nuclear medicine market progress along a different axis from past cancer treatment races (chemotherapy → targeted therapy → immunotherapy → cell therapy). Vertical Integration as decisive competitive advantage is unusual for pharmaceutical development — this is an area governed by competitive principles closer to manufacturing: “supply chain technology determines drug success.”

Three structural implications for the global ecosystem. First, isotope production becomes strategic infrastructure. Beyond the leading reactor sites (Belgium IRE, Netherlands NRG, Russia Rosatom), new commercial-scale ¹⁷⁷Lu and Ac-225 production facilities are being built across the US, EU, and Asia. National-level investment in isotope production is becoming as important as semiconductor fabrication for medical sovereignty. Second, the “subcategory of biopharmaceuticals” boundary is dissolving. Nuclear medicine, mRNA-LNP-based gene therapy, and CAR-T cell therapy all increasingly resemble each other in requiring vertically integrated, time-critical, highly engineered platforms. The 2030s-2040s biopharmaceutical industry will be defined by these intersecting modalities. Third, regulatory convergence is critical. FDA’s RPP (radiopharmaceutical) review pathway, EMA’s ATMP designation, PMDA’s regenerative medicine framework, and emerging APAC pathways — alignment of these frameworks will determine which markets receive new nuclear medicines first.

2026 is the year AI is rapidly commoditizing knowledge work. Nuclear medicine sits squarely in the “AI cannot replace” zone — physical isotope production, regulatory navigation, manufacturing infrastructure. This is precisely the type of frontier where leadership requires sustained capital investment, multi-decade R&D, and cross-disciplinary expertise. The next 5-10 years will see nuclear medicine evolve from specialty market to a major axis of cancer treatment.

Coming Next

Volume 2 dissects the major nuclear medicine competitors — Lantheus, Bayer, Telix, Point Biopharma successors, and emerging biotechs — comparing technical differentiation and industry reshuffling scenarios.

Edited by the Morningglorysciences team.

Comments